Guest Post by Profs. Masur & Ouellette: Public Use Without the Public Using

Guest post by Professors Jonathan S. Masur (Chicago Law) and Lisa Larrimore Ouellette (Stanford Law).

What is it that makes a use “public” for purposes of the public use bar? Does it matter whether the person doing the using is a member of the public, as opposed to the inventor? Or does it matter whether the use is itself in public, as opposed to taking place in secret behind closed doors? As it turns out, the answer to both questions is “yes,” but the questions are not as distinct from one another as that formulation might make it seem. Instead, the issue of who is doing the using turns out to affect where and how that use must occur if it is to be public use.

Begin with the question of who is doing the using. Most cases of “public use” have involved use by at least one member of the public—“a person other than the inventor who is under no limitation, restriction or obligation of secrecy to the inventor.” And when an invention is in use by a member of the public (rather than the inventor), it is blackletter law that the use can be “public use” even if it takes place entirely in secret, behind closed doors. In addition, it is also blackletter law that the use need not enable the invention to constitute prior art. No member of the public needs to see all the details of the invention or be able to reproduce it—it is enough that at least one person has come to rely on the availability of the invention free from any patent-based restriction.

But as we explain in a forthcoming article, a small line of cases suggests there is a second route to public use: even if no member of the public uses the invention, an invention can be placed in public use if it is used by the inventor, but only if it is displayed to the public in such a way that the relevant public could have understood the invention. That is, there can be public use without the public using, but only if that use is out in the open and with something like an enablement requirement. See Real-World Prior Art, 76 Stan. L. Rev. (forthcoming 2024). These cases appear to rely on an idea of constructive public knowledge: just as a conference poster can be invalidating printed publication prior art if a researcher could have learned about the invention by reading it, an inventor’s demonstration of an invention can be an invalidating public use if someone could have learned about the invention from observing the demonstration. Likewise, the Federal Circuit has held that display of an invention is not public use “if members of the public are not informed of, and cannot readily discern, the claimed features of the invention.” The only exception to these rules has come when the inventor is engaged in secret commercial use of the invention. Some courts have held that this puts the invention into public use. But more recently, the Federal Circuit has instead begun to hold that this places the invention on sale, because the whole point of the use is to exploit the invention commercially. We agree with the Federal Circuit panels that have held that the on sale bar is a better fit in these situations.

The upshot from these two lines of precedent is that the question of whether an invention is in public use depends intimately on who is doing the using. If the user is someone other than the inventor, then there is public use (a) even if the use is taking place in secret, and (b) irrespective of whether the user can figure out how the invention works (enablement). But if the inventor herself is the one doing the using, then (a) the use must be taking place in public, and (b) the use must be enabling.

As one might predict, the grouping of these two approaches under the single heading of “public use” has led to confusion among litigants and, in some cases, courts. Two new Federal Circuit decisions this month add to this “public use without the public using” line of cases and demonstrate the pitfalls of failing to keep the interlocking public use rules straight. In Minerva v. Hologic, the court held that display and demonstration of a medical device at a gynecological trade show constituted public use. The patentee, perhaps misunderstanding this line of doctrine, argued that it could not be public use because no member of the public used the invention. But the court held that “public use may also occur where, as here, the inventor used the device such that at least one member of the public without any secrecy obligations understood the invention.” Similarly, In re Wingen held that display of an inventive “Cherry Star” flowering plant at a private Home Depot event placed the plant into public use. The patentee argued that the display did not disclose the claimed genetics of the plant—which could have been a successful argument given the enablement-like inquiry imposed on other similar cases—but the court held that this argument was forfeited because it was not raised in proceedings below. It seems likely that the lawyers who argued the case before the PTAB had not thought to make this argument because they did not realize that use by the inventor requires enablement. Our article includes numerous examples of district courts that were similarly confused by the rules that vary depending on who’s doing the using.

As we explain in our article, treating enabling demonstrations by the inventor as prior art makes sense as a matter of patent policy. But lumping these cases under the “public use” umbrella has created confusion and mistakes among the lower courts. Going forward, we think the Federal Circuit should be explicit that there are two distinct routes to public use: (1) use by a member of the public—someone under no obligation of confidentiality to the inventor—which can take place in secret and need not be enabling, and (2) use by the inventor, which must take place in public and enable the invention.

Alternatively, and perhaps even better, the Federal Circuit could decide that the inventor-use category of activities instead implicates the “otherwise available to the public” prong of § 102. An enabling demonstration, where the public learns about the invention but cannot use it, could be the paradigmatic example of an activity that makes an invention available to the public without creating any other type of prior art. This is not a full solution given all the pre-AIA patents still in force, and in light of the strong policy reasons for barring pre-AIA patents that were displayed publicly we can see why courts have tried to fit these cases within the “public use” category. Regardless, for patentees and their attorneys, Minerva v. Hologic and In re Wingen serve as a reminder to avoid disclosing the details of an invention before they are ready to file a patent application—and if a disclosure does occur, they should remember to preserve the argument that it wasn’t actually enabling!

Patently-O Bits and Bytes by Juvan Bonni

Federal Circuit: System is Not a Method (and therefore patent must be delisted from Orange Book).

Federal Circuit Gives Stare Decisis Effect to a Judgment of Claim Validity

Guest Post: Third-Party Litigation Funding: Disclosure to Courts, Congress, and the Executive

Guest post by Jonathan Stroud. Stroud is General Counsel at Unified Patents – an organization often adverse to litigation-funded entities.[1] He is also an adjunct professor at American University Washington College of Law.

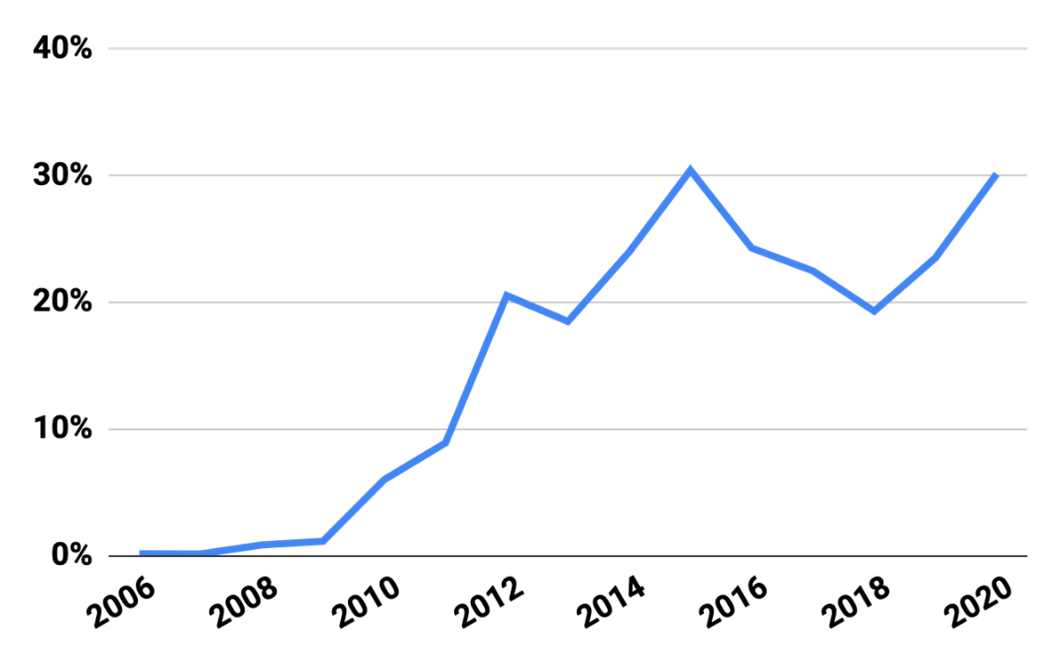

Patent assertion finance today is a multibillion-dollar business.[2] Virtually nonexistent in the patent space in the U.S. ten years ago—at least in part due to longstanding common law rules on champerty, maintenance,[3] and patent law’s relative high risk—today third-party litigation funding (TPLF)[4] undergirds about 30% of all patent litigation, by conservative estimates.[5] Insurance options are suddenly plentiful,[6] funders are expanding and multiplying,[7] and new deal commitments are on the rise.[8] This general trend is seen in the first chart below, adapted from a recent white paper by Korok Ray.[9]

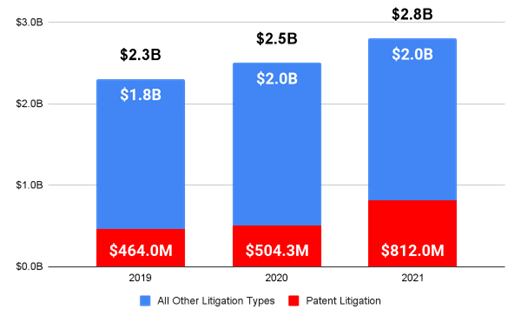

That is in no small part due to it being the fastest-growing piece of the wider U.S. litigation finance boom of the past 20 years—as has been widely reported, private equity now undergirds huge swaths of U.S. bankruptcy, class action, trademark, securities, and tort litigation, to the tune of $50 to $100 billion in investments annually.[10] According to one of the biggest litigation funders, publicly traded Burford Capital—recently featured on 60 Minutes[11]—there was a 237% increase in overall litigation funding in the US between 2012 and 2018, a trend that, by all accounts, continues unabated.[12] Industry reports show new investments pouring fastest into patent infringement litigation; new deal commitments for TPLF saw an increase of 61%; and patent litigation accounted for 29% of all new commitments by TPLFs in 2021.[13] Recent trends are shown in the chart below, adapted from a Westfleet Advisors report. [14]

In terms of how TPLF is structured, deals are variegated, complex private agreements. But generally the funder will offer non-recourse funding (or funding that is “at risk”) upfront to cover expenses in exchange for being first in line to recoup all of that funding first (i.e., to be “paid back”) out of any recovery, and then to take some hefty percentage—often 60% or more of whatever is remaining, particularly in litigations deemed high-risk (like patent litigation), though there are no rules governing how much funders can ask for. (It generally amounts to more than 50% of the total settlement recovery, acknowledging, at least by basic math, that they are the primary beneficiary of the litigation.). Sometimes all fees are paid upfront by the funder (Fortress is known for this); some pay some continuing level of a fee/contingency split with firms to split risk; some pay the original patentholder upfront, though others think that disincentivizes them from robust ongoing participation; others make all recovery, for all parties in a waterfall, contingent upon settlement. Many start with and later add investors to ongoing funds and matters. Nearly all require oversight and consultation at all key decision points.

Patent TPLF funds generally promise roughly 20% internal rates of return to funders (IRR) year-over-year, or about a 2x to 2.5x return on investment over generally four- or five-year investment cycles, suggesting, at least at the pitch level, that these investments are lucrative for the funders.[15] The biggest (or at least most well-known) players—Magnetar Capital, Burford Capital, Fortress Investment Group, Omni Bridgeway, and Curiam Capital, to name just a few[16]—have funded patent cases for years, reporting in some cases that their existing funds were on pace to return 20% or more—less than some other investments tout, but still beating the market by a fair margin.[17]

At least, that’s as far as can be pieced together. What we do know comes mostly from self-reporting, industry reports, and journalists. That’s because current disclosure of litigation funding relies on a patchwork of state law, court rules, self-reporting, FOIA requests, leaks to journalists, and funding pitches. It’s true today that no one in the government (Federal or state, judicial, legislative, or executive) knows who is funding which litigations, whether they are as profitable as they claim to be, if they are being properly taxed, or even how they are generally structured. Disclosure is limited even for the two well-known, publicly traded litigation fund managers, Burford Capital and Omni Bridgeway; it is sparser still—and highly self-selective—for all the private funds involved. According to a recent Government Accountability Office (GAO) report on litigation funding (written at Congress’ behest), “[e]xperts GAO spoke with identified gaps in the availability of market data on third-party litigation financing, such as funders’ rates of return and the total amount of funding provided,” and noted that no government body is aware of who is funding these cases, who is influencing or controlling them, or what promises they are making to investors.[18] (It also notes litigation finance industry lobbying groups active today, and their membership.)

Disclosure remains sparse at least in part because the very wealthy private investors who fund litigation claims and then reap, they claim, windfall profits—some of them concededly foreign sovereign nation funds[19]—have fought hard to keep those agreements secret, even from judges asking for disclosure, much less from government officials, researchers, reporters, opposing parties, or the public. As such, the Federal District Court of Delaware has recently found itself at the center of this high-stakes debate about transparency and the purpose of the courts.

In April of 2021, the District of Delaware’s Chief Judge, Colm Connolly, issued two standing orders requiring litigants to, inter alia, disclose third-party litigation funding.[20] (The orders apply to all parties and litigation before his Court, not just parties to patent disputes, but do not extend, as yet, to the other sitting judges there.) The orders were neither ultra vires nor exceptional—The Federal Rules of Civil Procedure have been moving toward greater ownership transparency for years, the advisory committees have recommended that judges have the right to such disclosure and are considering further requirements,[21] and similar requirements in Federal District courts across the nation have been in place for years, in districts in, for example, California, Georgia, Iowa, Maryland, Michigan, Nevada, New Jersey, Ohio, and Texas (in the Western district).[22] But that trend toward disclosure had thus far largely avoided being raised and enforced in the few Federal districts where patent litigation primarily resides (though the California and Texas districts have long had rules requiring disclosures—ones that are often ignored by LLC PAEs).